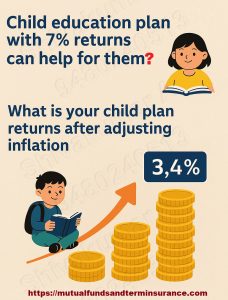

Child plan is sufficient for their education?

Planning for your child’s education or marriage, especially over a long-term horizon of 15 to 18 years, requires smart financial decisions. One of the most effective and flexible options available today is investing through child mutual funds, particularly equity-based mutual funds.

Thank you for reading this post, don't forget to subscribe!Unlike traditional child insurance plans, mutual funds focus entirely on wealth creation. They don’t come bundled with life insurance, which often includes mortality charges—an unnecessary cost when your primary goal is to save for your child’s future. These hidden charges can eat into your investment returns without offering any real value.

Parents often realize late that insurance plans marketed for child education are more of insurance products with low returns, rather than solid investment tools. Instead of mixing insurance with investments, it is wiser to separate the two.

Take a term insurance policy for yourself based on your lifestyle, income, liabilities, and future commitments. Term insurance is affordable and offers high coverage without the investment fluff. Then, invest separately in child mutual funds—especially SIP in diversified equity funds—which historically have delivered 12%–15% CAGR over the long term.

Education Inflation in India – June 2025

-

All-India combined education inflation reached 4.37% YoY in June 2025, up from 4.12% in May The Times of IndiaTrading Economics+9domain-b.com+9DD News+9.

-

For comparison, overall CPI inflation was just 2.10% in June – a six-year low The Times of India.

Bottom line: Education costs are rising significantly faster than general inflation, at about 4.4% annually.

🧮 Does Your Child’s Education Plan Outpace This?

If your education savings plan (like a child plan, ULIP, PPF, or SIP-based investment) offers a compound annual return above 4.37%, it will outpace the rising cost of education. Below are typical instrument returns for a 15–18 year horizon:

Common Investment Returns

-

Public Provident Fund (PPF): ~7.1% p.a., compounded annually Wikipedia.

-

Bank Fixed Deposits: Current rates ~6.5–7.0%, compounded annually.

-

Equity Mutual Funds (SIP over long-term): ~12–15% p.a. historically—but with volatility.

-

Children’s Education Plans/Insurance: Typically yield 5–7%, depending on product.

📈 Compound Growth Over 15–18 Years

Let’s illustrate with PPF at 7.1% p.a., compounded annually:

-

After 15 years:

Growth factor = (1 + 0.071)^15 ≈ 2.80×

Real growth over education inflation (4.37%) = net factor ≈ (1.071/1.0437)^15 ≈ 1.46× -

After 18 years:

(1.071)^18 ≈ 3.38×

vs inflation-adjusted: (1.071/1.0437)^18 ≈ 1.64×

➡️ You’d beat education inflation by about 46–64% over the term.

If you choose equity funds (say 12% p.a.):

-

(1.12/1.0437)^18 ≈ 2.55× real growth—a substantial cushion above rising fines.

Why Child Mutual Funds Are the Smartest Choice for Your Child’s Future

Mutual funds offer transparency, liquidity, tax efficiency (especially under long-term capital gains), and professional fund management. They also benefit from compounding, which becomes powerful over 15 to 18 years.

In summary, don’t fall for emotional insurance pitches that cost more and give less. Choose mutual funds for growth and term insurance for protection—a winning combo for every smart parent.

📞 Call Shivakumar A – 9480240513 for a customized education and marriage planning strategy tailored to your goals.

⚠️ Points to Check in Your Plan

-

Effective compound rate vs nominal: what’s the actual accrued rate after fees and compounding?

-

Lock-in duration: Most child plans lock funds for 15–18 years—fits your horizon.

-

Flexibility & Taxation: Compare maturity payout structure, indexation on withdrawals, and tax impact.

✅ Summary

-

Education cost inflation: ~4.37% as of June 2025.

-

To stay ahead, your plan needs > 4.4% p.a. compounded returns.

-

PPF (~7.1%), FDs (~6.5–7%), and ULIPs/SIPs (~8%+) typically outperform this, long-term.

📞 Want Expert Guidance?

Reach out to Shivakumar at 94802 40513 — he can assess your current education plan’s performance and help align it to beat inflation, advising on compounding returns over your 15–18 year goal.