Never Mix Insurance and Investment

In the world of personal finance, one golden rule stands tall: Never mix insurance with investments. Yet, many people fall into the trap of combining the two, primarily through endowment or money-back insurance policies. These products promise both life coverage and a return on investment, but they usually underdeliver on both fronts. If your goal is to protect your family and grow your wealth, you’re better off separating insurance and investments.

Thank you for reading this post, don't forget to subscribe!

Buy Term Insurance: Pure Protection at a Low Cost

Term insurance is the most straightforward and cost-effective form of life insurance. It provides a high sum assured at a low premium, offering financial protection for your family in case of an untimely demise. Unlike traditional endowment policies, term insurance doesn’t promise maturity benefits. And that’s a good thing.

Because you’re not paying for an investment component, term plans are cheaper and offer better coverage. For example, a 30-year-old can purchase a ₹1 crore term policy for as little as ₹8,000 to ₹10,000 annually. The remaining money, which would otherwise be locked in an underperforming endowment plan, can be invested in high-return avenues like mutual funds.

Here is why – Never Mix Insurance and Investment

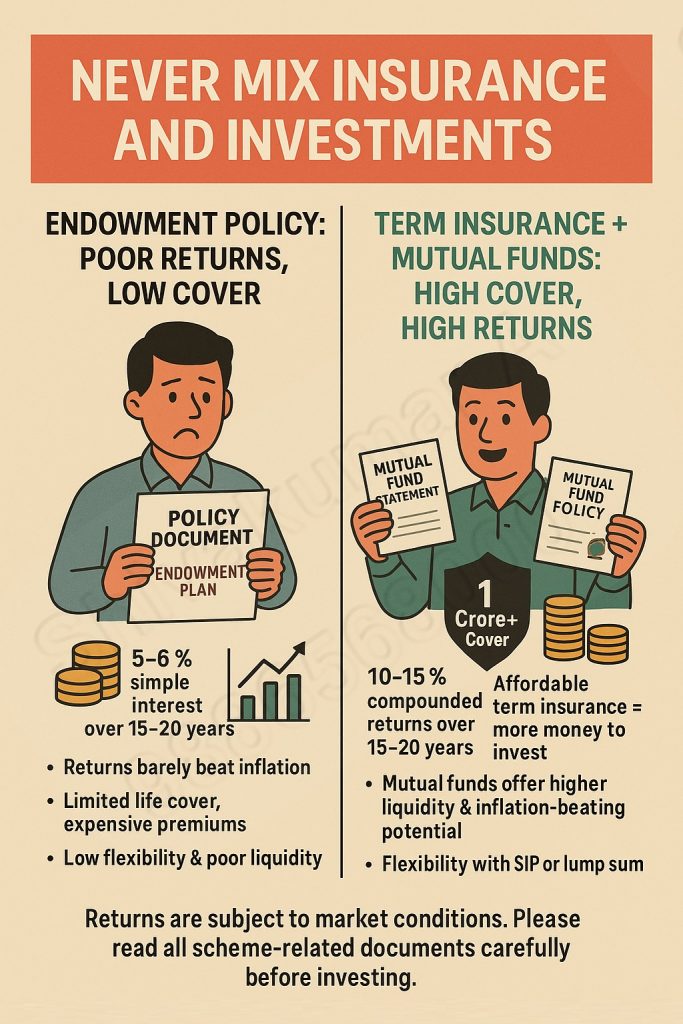

Endowment Plans: Low Returns, Long Lock-ins

Endowment plans may seem attractive because they offer both insurance and returns, but the numbers tell a different story. Most endowment or traditional life insurance policies yield around 5% to 6% simple interest over a 15 to 20-year period. When adjusted for inflation, the real return is even lower, often barely enough to beat rising living costs.

Additionally, these plans are illiquid. If you try to exit early, you could lose a significant portion of your investment. The rigid structure and poor returns make endowment plans a poor choice for long-term wealth creation.

Mutual Funds: Inflation-Beating Potential

On the other hand, mutual funds—particularly equity mutual funds—offer the potential to earn 10% to 15% compounded annual returns over the long term. These returns not only outpace inflation but also significantly grow your wealth due to the power of compounding.

You can invest in mutual funds through:

-

SIP (Systematic Investment Plan): A disciplined approach where you invest a fixed amount regularly, taking advantage of rupee cost averaging.

-

Lumpsum: Ideal when you have a large sum available to invest at once.

While mutual fund investments do carry market risk, they have historically outperformed traditional instruments over 10–15 years. They are also highly flexible—you can increase, decrease, or stop your investments at any time.

Disclaimer: Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing.

A Simple Strategy for Smart Investors

Here’s a simple and effective financial strategy that separates insurance from investment:

-

Buy a term plan for your life cover needs.

-

Invest the savings (from not buying expensive endowment plans) into mutual funds, either through SIPs or lump sum investments.

-

Stay invested for the long term to maximize the benefits of compounding and ride out market volatility.

For example, if you save ₹50,000 annually by opting for term insurance over an endowment plan and invest that amount in mutual funds, at a 12% annual return, you could accumulate over ₹20 lakhs in 15 years.

Why Term life insurance with Mutual funds

Never mix insurance and investment—doing so often leads to compromising both. to beat inflation, Insurance is meant purely for protection, while investment is for wealth creation. Combining them in products like ULIPs or endowment plans often results in low returns and inadequate coverage. The smarter approach is to separate the two: buy a pure term insurance plan to secure your family financially, and invest in mutual fund SIPs based on your risk profile and goals. This way, you get high life cover at a low cost and potentially higher returns from investments. It’s the most efficient and flexible way to plan your finances.

Never Mix Insurance and Investment: Keep It Simple, Keep It Separate

Combining insurance and investment may seem convenient, but it often results in subpar returns and inadequate protection. By keeping insurance and investment separate, you ensure that your loved ones are financially secure while your money works hard to grow over time.

Choose term insurance for affordable life cover, and invest in mutual funds to build wealth and beat inflation. Avoid endowment plans that offer low returns and limited flexibility. Make informed choices, read offer documents carefully, and consult a financial advisor if needed.

The road to financial freedom is paved with smart, informed decisions—and it starts with separating insurance from investment.