Why Mutual Funds are better than ULIPs? Check now

Mutual Funds and ULIP have a long relationship, but both represent a big difference in earnings. Our Investments can be categorized largely into two verticals. ULIPs seem to be very simple in investing as the company does its work and gives returns to the investor with Life Insurance cover. Whereas Mutual Funds are invested directly by the investor as they believe in the brand and the Fund Manager.

Thank you for reading this post, don't forget to subscribe!When it comes to investing for long-term wealth creation, many people are confused between Mutual Funds and Unit Linked Insurance Plans (ULIPs). While ULIPs claim to offer the dual benefit of life insurance and investment, the reality is often far from ideal. In comparison, Mutual Funds are a more transparent, flexible, and cost-effective option for building wealth. Let’s understand why Mutual Funds are better than ULIPs in almost every aspect.

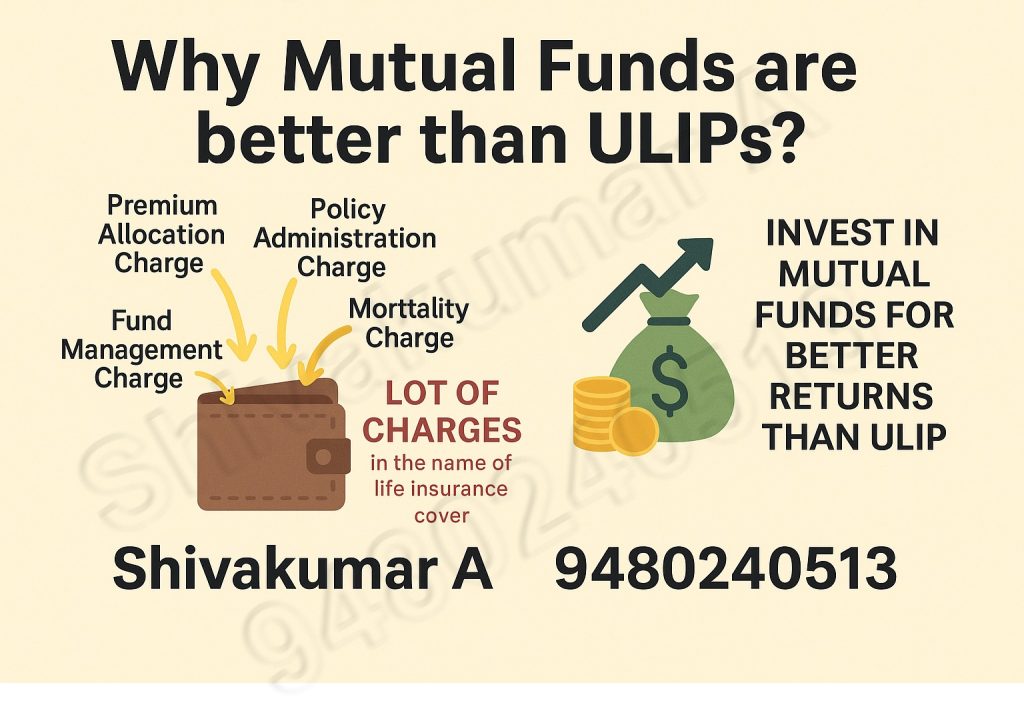

ULIPs Have High Charges – Up to 25-30% in the First Year

One of the biggest drawbacks of ULIPs is their high upfront charges. In the first year alone, charges can eat up 35% to 40% of your premium, which means only 60% or less is actually invested on your behalf. These charges include:

Premium Allocation Charges

Policy Administration Charges

Mortality Charges

Fund Management Charges

Surrender Charges (if you exit early)

On the other hand, Mutual Funds come with much lower expense ratios, usually around 1–2% for actively managed funds and even lower for index funds. The money you invest in mutual funds is fully utilized to buy units in the fund, offering much better compounding and returns.

Check before investing in ULIPs

ULIP Life Insurance Coverage Is Very Minimal

While ULIPs are marketed as a combination of investment and insurance, the insurance cover offered is often inadequate. For example, a person paying ₹1 lakh premium per year might get a life cover of only ₹10–15 lakhs, which is not sufficient for a family’s protection.

Instead, if you separate investment and insurance, you can:

Buy a term insurance plan for around ₹20,000 per year and get ₹1 crore coverage.

Invest the remaining ₹90,000 in mutual funds to grow your wealth.

This strategy is known as “Buy Term, Invest the Rest” – and it works far better than putting all your money in a ULIP.

ULIPs Have a 5-Year Lock-in Period

ULIPs come with a minimum lock-in period of 5 years, which means you cannot withdraw your money in case of emergencies or changing needs. Even after the 5th year, there may be surrender penalties or restrictions.

Mutual Funds, especially ELSS (Equity Linked Savings Scheme), have a shorter lock-in of just 3 years, and other types of mutual funds like equity or debt funds have no lock-in at all (except tax-saving funds).

This flexibility allows mutual fund investors to manage their money better according to life goals and market conditions.

Returns in Mutual Funds Are Generally Higher

Since mutual funds have lower charges and professional fund managers, the returns are generally higher compared to ULIPs. ULIP returns are diluted by multiple hidden charges and a lack of aggressive investment strategy.

Moreover, mutual funds offer a wide range of options – large-cap, mid-cap, small-cap, balanced, debt, index, international – allowing investors to build a diversified portfolio based on their risk appetite and goals.

Transparency and Regulation

Mutual Funds are regulated by SEBI, and all fund performance, portfolio details, and expenses are disclosed regularly. ULIPs, on the other hand, are insurance products and fall under IRDAI, but are often marketed aggressively with limited transparency.

Summary

ULIPs may seem like a convenient product that offers both insurance and investment, but in reality, they come with high charges, low returns, inadequate insurance cover, and long lock-in periods. Mutual Funds offer better flexibility, transparency, and higher potential returns.

The smart way to build wealth is to keep insurance and investment separate. Buy a term plan for protection, and invest in mutual funds for growth. Don’t let marketing gimmicks and complex charges trap your hard-earned money. Invest smart. Invest in Mutual Funds.

ULIP Charges you should know before starting the investments

The investor needs to come to a conclusion that he wants to invest or insure. Keep Insurance and Investments separate. Term Insurance and Mutual Funds combination is the best type of investment to beat inflation. If you are very particular and don’t want to take risks, better would be Endowment plans. Mutual Funds are less expensive than ULIPs. Most of the Unit Linked Insurance Plans are loaded with many kinds of expenses like allocation charges, mortality charges etc.

Invest in the best Mutual Funds after comparing, call 9480240513

*Mutual Funds returns are subject to market conditions, Please read the offer document before investing.